When you hear “blockchain,” you might immediately think of Bitcoin. But the world of blockchain is more diverse than just one flavor. Understanding the different types of blockchains is key to grasping their varied applications and functionalities. Let’s break down the main categories:

1. Public Blockchains: The Open Networks

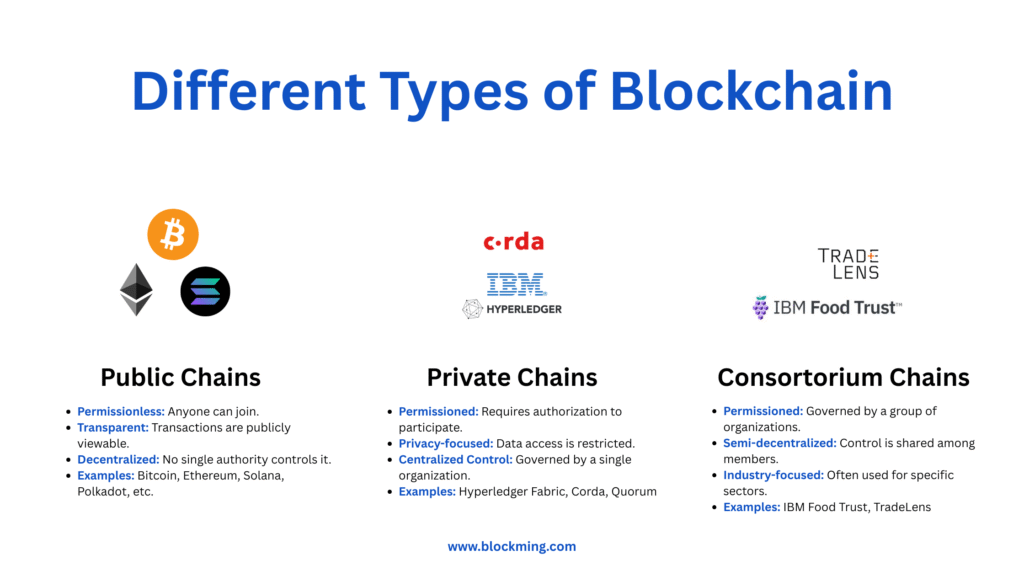

Think of public blockchains as completely open and permissionless networks. Anyone can participate – view transactions, send transactions, and become a validator (depending on the consensus mechanism). They’re all about transparency and a high level of decentralization.

- Bitcoin: The pioneering cryptocurrency that introduced blockchain technology. Often referred to as digital gold.

- Ethereum: A platform enabling smart contracts and decentralized applications (dApps). Powers a vast ecosystem of decentralized finance and NFTs.

- Polkadot: Aims to connect different blockchains, enabling interoperability and scalability. Focuses on creating an internet of blockchains.

2. Private Blockchains: Permissioned & Controlled

In contrast, private blockchains are permissioned networks. An organization controls who can participate and access the data. These are often used by enterprises for internal applications where privacy and control are paramount. Think of a company using a blockchain to manage its internal supply chain, where only authorized partners have access.

- Hyperledger Fabric: An open-source enterprise-grade permissioned distributed ledger framework. Designed for modularity and building customized blockchain solutions.

- Corda: A distributed ledger platform designed for regulated industries like finance. Focuses on recording agreements directly between parties.

Ethereum Enterprise (Quorum): A permissioned version of Ethereum tailored for enterprise use. Offers privacy enhancements for enterprise applications on the Ethereum network.

3. Consortium Blockchains: Collaborative Networks

These sit somewhere in between public and private blockchains. They are also permissioned, but instead of a single organization, a group or consortium of organizations governs the network. This allows for a more decentralized but still controlled environment, often suitable for industry-wide solutions like in the shipping or finance sectors where multiple stakeholders need shared, trusted data.

- IBM Food Trust: A blockchain network aimed at improving transparency and safety in the food supply chain. Provides end-to-end visibility in the food ecosystem.

- TradeLens (IBM & Maersk): A platform designed to streamline global trade and shipping processes. Digitizing and connecting the global supply chain.

- R3 Corda: Also used in consortiums, particularly in finance. Facilitates direct and trusted exchange in financial markets.

The application of blockchain in supply chains, whether through public, private, or consortium models, showcases the technology’s power to enhance transparency, efficiency, security, and traceability across various industries. While the world of cryptocurrencies brought blockchain to the forefront, it’s these real-world applications that highlight its transformative potential.

Related Frequently Asked Questions

- What’s the main difference between public and private blockchains?

Public blockchains are open to everyone, promoting transparency. Private blockchains are permissioned, offering greater control and privacy for specific organizations. - Why would a company use a private blockchain?

For enhanced control over data access and participation. Private blockchains can improve efficiency and security for internal operations and trusted partners. - Who’s in charge of a consortium blockchain?

A group of organizations jointly governs consortium blockchains. This model suits industry collaborations requiring shared trust and data management. - How does blockchain make supply chains better?

It provides a transparent and unchangeable record of a product’s journey. This boosts traceability, confirms authenticity, and reduces the risk of fraud. - Is blockchain only for cryptocurrencies?

No, while crypto was the initial big use case, blockchain’s secure and shared ledger system has many different applications across various industries.